New article

Recently updated

Using the Canada Controls database

Who is this article for?

Users who want to learn about the Canada Controls database.

No special access or permissions are required.

The Audit Analytics Canada Controls database covers all Canadian public companies filing assessments of disclosure controls and procedures and internal controls over financial reporting, as required by National Instrument 52-109.

1. Understanding common uses

The Canada Controls database helps you:

- Use controls as a factor to gauge financial reporting quality

- Prospect for business by identifying companies with financial reporting issues

- Filter controls by control effectiveness, revenue, and market cap

- Compare ineffective controls by industry type

The database is available online, through WRDS, and through data feeds [Feed66] with the relevant subscription. Saved Search Alert functionality is available, but Daily Summary Email is not.

2. Understanding collection methodology

Currencies are converted from the reporting currency using the exchange rate as of the corresponding event date (Market Cap Rate, Revenue Date, Assets Date, or fiscal year end, as applicable).

Note: In August 2024, the following fields were modified due to a change in source data: Industry Key and Industry Description were deprecated, and Business Phone, Business Fax, and Contact Fax were replaced by two new fields (Phone and Fax).

Venture Issues are not required to make representations relating to the establishment and maintenance of disclosure controls and procedures (DC&P) and internal controls over financial reporting (ICFR), as defined in National Instrument 52-109. Issuers that comply with SOX 302 and SOX 404 requirements are exempt from NI 52-109.

This data is sourced from the following form types: MD&A, MD&A (amended), annual information form, annual report, annual report (amended), annual report on Form 10-K, annual report on Form 20-F, audited annual financial statements, and audited annual financial statements (amended).

3. Searching the database

The Canada Controls search page offers multiple filters to refine your search results.

| Name | Description | Data Dictionary Field(s) | Sort By? |

| Auditors | Filter by fees for a specific auditor or group of auditors | Auditor Name Auditor Key | No |

| Issuer Number or Tickets | Filter results to a specific population | Issuer Number CIK Code Ticker | Yes |

| Search Control Text | Search for text containing keyword | N/A | No |

| Market Index | Filter by SEDAR Market Indices | Current TSX Issuer Current TSXV Issuer | No |

| Currency | Filter by representing currency in which audit fees were reported | Reported currency | No |

| Market Cap (CAD) | Filter by companies’ market caps | CAD Market Cap | Yes |

| Revenue (CAD) | Filter by companies’ revenue | CAD Total Revenue (MRFY) | Yes |

| Assets (CAD) | Filter by total assets as of asset date | CAD Total Assets | Yes |

| Filter by Industry | Filter by companies’ industry(s) | NAICS Code | No |

| Company Location | Filter by current business address location(s) | Bus City Bus State Bus Country Bus Code | No |

| Period End | Filter by a range of dates to return on corresponding controls information | Period End Date | Yes |

| File Date | Filter by a range of dates of when source filing was submitted to SEDAR | Filing Date | Yes |

| Effective Controls | Indicates whether management’s disclosure contains reference to existing material weakness | Controls are Effective | No |

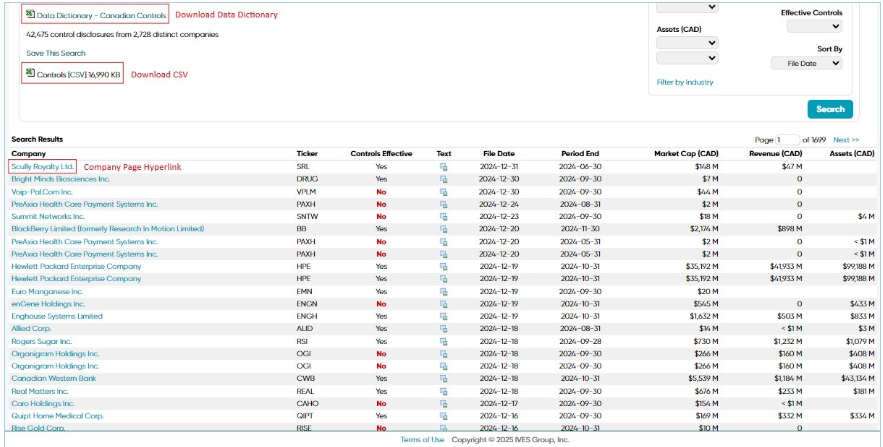

4. Viewing and exporting results

Results appear at the bottom of the page. You can access the following through the respective hyperlinks:

- Canada Controls Data Dictionary download

- CSV file downloads of the results (all fields available in the CSV are defined in the Data Dictionary)

- Overview of individual companies' profile

5. Understanding national instrument 52-109 requirements

National Instrument 52-109 requires certifying officers to establish and maintain a system of effective disclosure controls and procedures (DC&P) and internal controls over financial reporting (ICFR) that would provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with the issuer's generally accepted accounting principles (GAAP).

If an issuer identifies material weaknesses in the design of ICFR, the issuer is required to provide a description of the material weakness, the impact that the material weaknesses may have on the financial reporting, and any plans for remediating the weakness.